Golden Futures

By Orit Halpern

In Northern Quebec in the region of Abitibi lies the Malartic gold mine. The largest open pit gold mine in Canada, it is a vast expanse of land. The pit itself is approximately 4 km wide, the entire mining field is 23km2. Standing at its edge, one can envision what it might mean to inhabit another planet. For this is an inorganic environment. We may speak of the Earth in metaphors of care, life, and love, but in reality almost all the Earth, beneath the very thin strata of top-soil upon which the biosphere rests, is violently anti-pathetic to carbon based life forms. Metals and minerals quickly turn acidic and poisonous when they enter the biosphere. Life sustaining substances like water and air, are the very reagents to facilitate oxidation; turning rocks into agents of acidification and destruction of the biological environment.

We have not however, like the Greek myth of King Midas, yet learned to curse these gifts borne from this most valuable metal. It is said that Midas turned his own nourishment into gold, realizing then it was a curse. But in contemporary mining what might appear as something to choke on, mainly the toxicity of mining to life, is eternally deflected through chemistry, logistics, and derivation.

Chokepoint takes numerous valences here. First, there is the literal choking of life, the accumulation of materials that are toxic to the ecology within which the mine exists; terminally threatening the surrounding ecosystems and potentially inducing the literal stoppage point to life, itself, or at least certain forms of life. The second form of stoppage, is the limit to resources, thegold will inevitably run out. The mine is therefore a mortal creature, whose life expectancy is short. The third chokepoint lies in value, and capitalist accumulation. The end of gold induces particular concerns for markets and for speculation; inducing a constant hunt for new reserves and new resources and a regular hoarding of existing resources. Fourth, exploration and extraction are themselves constant chokepoints in the productivity and profitability of the mine. Exploration costs the most, guarantees nothing, and takes time. All these locations of stoppage, slow down, and accumulation—of life, economy, and resources—gesture to the future present tense of the mine. The mine has many temporalities—geological, technical, financial, and organic—and extraction industries mitigate and use these multiple temporalities, and even jams, to evade the ultimate endpoint—resource depletion and extinction. The mine is thus an assemblage of chokepoints—limits to resources, to sustainability and environmental health, and to logistics—that are averted through a series of technical tricks that manage time and flow to avoid encounter with ever choking on all the waste that mines produce.

In the course of this brief essay, I will lay out the different, yet deeply entangled strategies, by which encounters with terminal market failures and catastrophic environmental events are deferred through a new logic of ubiquitous computing merged with algorithmic capital. Zones. Logistics. Optimization. Datafication. Derivation. These are the steps by which extraction infrastructures avoid choking on their own accumulated detritus of heavy metals and toxins by turning it into leveraged futures and credit-debt swaps. Data and Derivation have become global computational strategies to avoid terminal failures of security, ecology, and economy while also turning the future into a hedged bet on life on earth orchestrated through our machine systems. In the face of earthly finitude we turn to informatics overload.

Zones

“Quebec is for mining, what Switzerland is for banking…a free trade zone,” the geo-engineer in charge of dealing with monitoring hydrology and water acidity and toxicity entering the environment confided to me. There are, indeed, many mines along the Canadian shield, a vast expense that stretches across Canada up to the Arctic. Millions of years ago a glacier swept out the top levels of the earth, leaving the previous minerals and metals exposed, ripe for the picking. But the picking is no longer quite so ripe. “There is no more easy mining on earth”, the lead mine reclamation geologist at the site, Dr. Mostafa Benzaazoua, informed me. All the metals and energy sources on Earth will be depleted, he predicted, by 2155. This is even if we account for envisioned improvements in technology. As a result, mining has become about chemistry and derivation. Mining literally uses chemical processes, in the case of gold, cyanide, to bind with the ore and remove it from the waste rock. The same is true for most other metals, using different agents to extract the metal from the rock. When ore deposits were better, other processes, such as heat could be used. But in today’s world, all extraction has turned to chemistry. In turn, there is a massive amount of tailings ponds, that are both toxic but also sites of “mining” for further possible value through new chemical and technical processes that might derive more ore, or find other metals and mineral of worth in the waste. All of this must happen within the relatively short times concessions last, driving a constant effort to derive more value from the site, and constant operations. The mine works 24/7 everyday. No stoppage allowed. At the same time, gold is literally used to ground many credit derivative markets, literally becoming a derivative itself. In the face of shortage, we turn to logistics.1

Logistics

Despite the barren terrain, this mine is also lively. And in our technical age, there are many forms of life. The mine is constantly in action, moving in rhythms that Marx might have labeled “metabolic”. Operating without stop, the mine extracts 55,000 tons of rock a day. This rock is moved, tested, and then separated into ore rock and waste rock. The rock with ore will go to a processing plant that will remove the gold, while the rest is immediately laid to rest in the some 20km2 of tailing ponds that lie behind the installation. The mine is a logistical masterpiece. Vast machines lumber through the space carrying their rocks in stately well-timed rhythms. These large behmouths are perfectly synchopated through the Caterpillar software platform that tracks the movements of these vast machines, the amounts and speed with which they carry their loads, and times their loading, unloading, and maintenance. Each truck costs $3 million dollars, each tire is 11 feet high and costs $42,000 to replace. The tires last 8 hours of driving. The entire mine has a short life. It is anticipated to only last another approximately 15 years (its entire life will have been 27 years), the concessions do not last longer, and the ore is running out. It is necessary therefore to optimize every operation. These time scales seem paltry in comparison to the geological formations the mine has unearthed, and the vast new territory it has produced in both time and space.2

Optimization

Mines, I was informed, are no longer seen as stable sites, but rather as time-bound organisms, with life spans and afterlives. Since the 1980s when Canada began requiring some efforts at mine reclamation and environmental clean-up (that ironically timed with the moment that major mining corporations benefited from structural readjustment and neo-liberalism in the Global South) the design of mines has changed.3

In turn, mine design must now take into account both global supply chain and markets, in real-time, and the life cycles of their localities. As Dr. Benzaazoua explained, mines now must submit proposals for reclamation, and plan for their clean-up when filing their request for a concession in Quebec. Their engineering and design from the start, already assuming their impending death and resurrection, and in this arguably, there might be opportunity, for good or bad, to have to contend with and imagine what it means to inhabit a toxic and damaged planet.

Mining companies today thus seek to do everything from turning tailing ponds into new resources for construction materials, to figuring out if the waste rock might not yet offer a different mineral or metal that might be extracted. There is a constant search to sift through detritus in the hope of turning “waste” into resource. The process must be constantly optimized in the present and into the future. As a result, the mine, Benzaazoua tells us, is a space “of flows”. Flows of capital, machinery, information, and materials. It is also a space of transformation, mining today is about chemically extracting the ore from rock. In the case of gold with cyanide; a process that leaves its own dangerous residues, and that must be carefully managed. This chemistry will facilitate the production of what once was alchemical—gold—and of markets.

Over 90% of what is mined at Malartic, and globally, will be re-placed underground into bank vaults. These standing reserves of unused gold will serve as a hedge bet against more volatile derivative and futures markets. Circulation seemingly capable of subverting or diverting this terminal chokepoint, the finitude of gold in the earth, to mining activity through speed.

Derivation

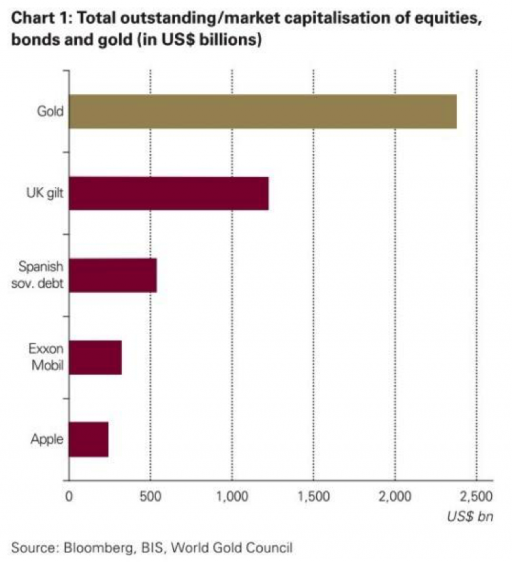

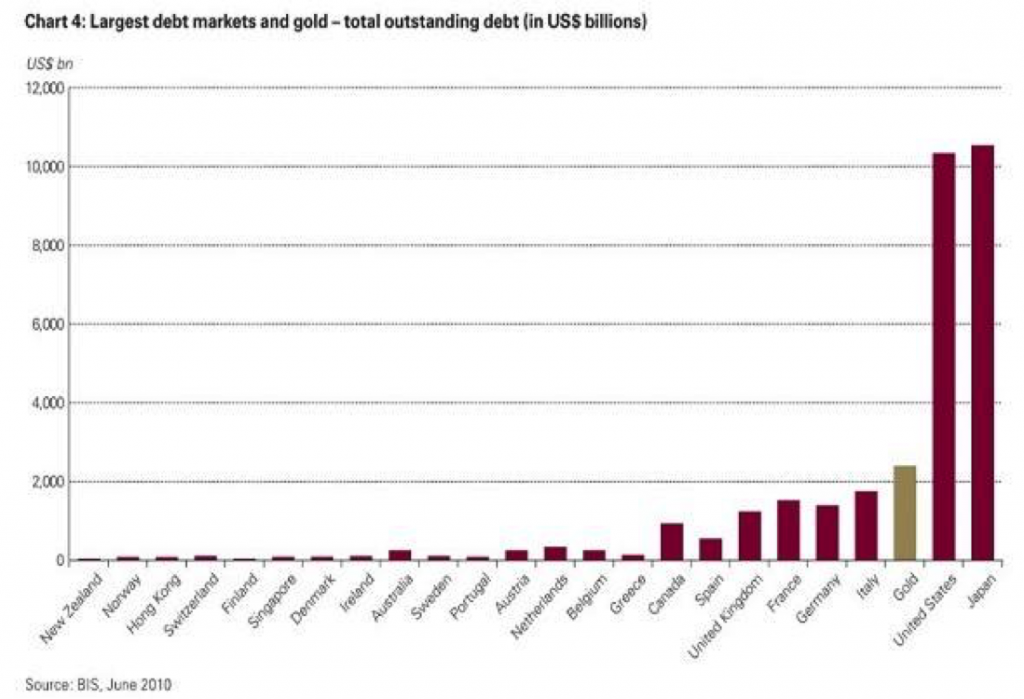

The biosphere might be in trouble, but it seems we are hedging our bets. The conduct of the mine mirrors the very logic of gold as that element historically always used to hedge a bet. The secure standard, even long after the demise of the gold standard and even the Bretton Woods accords, gold remains the standard benchmark for security in producing value. Gold markets as of 2010 were among the largest debt-hedging markets in the world. It is estimated that the derivative markets are betting on over ten times the annual new mine supply, and by now far more then official reserves. The markets exceed the reality of production exponentially; setting prices and making bets far into the future.4 As of 2015, gold markets were considered extremely important portion of the sovereign debt markets. As the 2008 market crash made evident, there are markets where debts and credit are swapped, betting on futures, potential return or even default. Gold often serves as “hedge” a guarantor and a standard of value. Gold markets overshadowed national debt markets such as the Spanish debt market of the time, that of most other nations, and far overshadowed even equity investments and other “hedge” entities like Exxon Mobile and Apple.5

Datafication

To achieve this seemingly sisyphean hedge-bet, we transform space into logistical movements grounded in a most literal connection between data mining and metal mining. The mine is covered by a network of information gathering sensors that monitor water, humidity, temperature, winds, atmospheric conditions, geological stability and topology. The datafication of this space represents the effort to monitor the location of ore, to secure the mine’s structural integrity, and to guard the city within which the mine is located, as well as the boreal forests and many acquifers, that are always at risk of coming in contact with the materials, metals, and minerals being removed from the Earth with such speed. The mine’s floor is lined with coring stations that attempt to unearth those locations where gold is in abundance. Abundance in this case being 1 ppm, which is to say one ton of rock is dug for 1 gram of gold. Such low amounts of ore demand constant blasting and excavation to produce anything worth selling. By the end of the mine’s life it will produce 580,000 ounces of gold, and 700,000,000 tons of waste rock.

All the gold, I was told by the mining operatives, that has ever been mined in the world could fill two Olympic swimming pools. This drives a constant searching for new veins of ore, a search that occurs through the air as well as through core sampling. First airplanes and satellites provide initial information on rock formations, structures, and features that might identify resource fields through electromagnetic survey, ground penetrating radar surveys, and often satellite imagery. There are also sensors on the site that monitor, survey, and assess every movement and shift of the earth. So much digging and blasting demands an array of sprinklers that constantly keep the site damp in an effort to control particles and dust from contaminating the air. The mine is unusual for being located literally in a city, and therefore its immediate impact on human health is of paramount concern. The mine also boasts research stations where geo-engineers attempt, perhaps futilely, to figure out how to guard all this waste rock from water which will subsequently turn the sulfides and other minerals and metals in the rock into acid. This would be lethal upon entering the surrounding boreal ecosystem.

Among the geo-engineers with which I speak, the discourse is medical, and the practices are surgical. The skin of the earth that has been peeled back is to be covered by a new molt of electronic information, literally evaluating and managing the membranes between the mine and its world. The mine is a contaminating entity, whose worst effects will be contained, through the speculations of geo-surveying, the imaginaries of mine reclamation, and the omni-presence of capital.

Speculation

Facing the limits to planetary resources and maybe life, we have turned to ubiquitous computing, geo-sensing, and algorithmic trading. To avoid these terminal chokepoints of resources and toxins, the mine must conquer the limits of space through deriving value from the future. Derivatives are financial instruments that allow a certain amount of something (mortgages, minerals, oil, anything) to be traded at some point in the future at an agreed upon price. One can also, for example, also bet on the cancellation of an order, or some other event changing the future price of the underlying commodity or security. 6

Futures derivative future markets make a double move. They bet change in value of some entity (you can even bet on the weather) between the present to some future point against another change in value of some other entity. But what makes the market interesting is that you can sell your bet before the event happens. In doing so, one “hedges” the future. And gold is the long standing hedge bet. You can pull out when you make money irrespective of what the future might hold.7 Time no longer equals money but rather money derives from time=time, from bets on relations between times. One can swap the debt, for example, on a package of mortgages, or of entire countries, for gold futures, without the homes being sold, or nations paying or defaulting on their loans. You are betting on temporalities of two different markets, looking to bet on fluctuations in price between the two markets. The forms of time here are speculative not predictive. One does not need to calculate the final risk of the action of investment; only manage the time of the action. Risk which is calculable has now become just raw uncertainty to be managed through algorithmic financial logics that mirror the big data infrastructures of the extraction industries themselves.

Such understandings of time, of course, demand that we ask: what is the relationship is between derivation and extraction? This logic takes its built form in a discourse of reclamation, optimization, and “sustainability” that now dominates mining and energy industries. The value of the mine is constantly being transformed through changes in the mines function and extractions of value from what before was waste. We are constantly sifting through the detritus of our destruction of the environment in search of increments of changing future values to bet on. What is true of gold, is also true of most other extraction industries, especially oil markets.8 We are turning the planet into a derivatives machine.

As future risk transforms into uncertainty through derivation, high technology, particularly “smart” and “ubiquitous” computing infrastructures become the language and practice by which to imagine our future. Instead of looking for utopian answers to our questions regarding the future, we focus on quantitative and algorithmic methods, on logistics, on how to move things, not on where they end up or on measuring the impacts of these actions. We have turned data into gold, and reverse, not as metaphor, but in practice. The result is the development of forms of financial instrumentation and accounting that no longer (need to) engage with, alienate, or translate, extraction from a historical, geological or biological framework of value. Our planet is now a hedged bet, where finitude in life is converted to surplus information for future speculation.

Uncertainty

This situation may not be hopeful, but it should not lead to despair. We must simply find forms that do not match the vacant speculations of our present. Environmentalists and indigenous land and human rights activists in Canada right now, for example, also seek change by attempting to change risk valuations on pipelines and other infrastructure projects by insurance companies, in order to increase the interest rates, and therefore the price of the project. Increasingly, many of us recognize that transforming the nature, time, and regulation of the bet, is the source of a difficult, but possible, alternative future. Despite being seemingly abstract and delinked from the present, derivatives also drive human actions.9 People build homes, take mortgages, build pipelines, and mines, and subsequently suffer when these markets move. By tying together disparate actions and objects into a single assembled bundle of reallocated risks to trade, derivatives make us more indebted both to each other and to the planet itself, which is often the literal matter of such exchanges.10 The political and ethical question thus becomes how we might activate this increased indebtedness in new ways, ones that are less amenable to the strict market logics of neo-liberal, perhaps now neo-extractionary, economics, all of which is algorithmically driven. All futures are bets, our task now is to open those risk assessments and extractionary hedge bets to the uncertainty that faces all life on earth.

Notes

1 I partook of this experience, as part of a research studio course I organized this past August through Concordia University in Montréal with Pierre-Louis Patoin from Sorbonne Nouvel 3. This material is taken from visits to malartic from August 2-5, 2017. Dr. Mostafa Benzaazoua, from the University of Quebec at Abitibi in the Research Institute in Mining and Environment, a mine reclamation expert was our guide and collaborator. I am grateful to his assistance and that of his colleagues in doing this research. On August 4 we were given a tour by the mine staff, whose names are being withheld as a matter of privacy.

2 All these numbers were recounted by mine employees on August 4, 2017.

3 The holding companies at Malartic Mines are Agnico Eagle and YamanaGold. YamanaGold is a Toronto based company that dates from 1980 and has holdings in Brazil, Canada, Honduras, Nicaragua, Chile, and Mexico. Agnico Eagle is an older Canadian firm from 1957, that expanded in the 2000’s into Finland and Mexico. Both do not trade directly in futures markets, as a result of burst in the market in the early 2000’s, but do sell to banks that then directly use this gold to hedge debt both central banks and investment banks. https://www.agnicoeagle.com/English/60th-anniversary/default.aspx http://www.canadianmalartic.com/Apropos-partenariat-en.html

4 The difficulty in pricing metals (also oil) as a result of derivatives markets has even led to mines owned by AgnicoEagle to advertise that they do not sell futures. While the mine may “guarantee” the price of its gold, however, the owners of the gold clearly do not as evidenced by the size of gold derivative and futures markets. https://www.agnicoeagle.com/English/60th-anniversary/default.aspx http://www.canadianmalartic.com/Apropos-partenariat-en.html

5 Dickson Buchanan, “Just How Big is the Gold Market?” August 5, 2015, https://schiffgold.com/commentaries/just-how-big-is-the-gold-market/ downloaded October 31, 2017

Henry Sanderson, “Traders Warn on Gold Liquidity”, Financial Times, May 18, 2015 https://www.ft.com/content/0b68ba36-f3f3-11e4-a9f3-00144feab7de downloaded November 5, 2017.

6 The result is that the size of the derivatives markets far overshadows the actual world’s gross domestic product, by now exceeding the world’s GDP by twenty times. These markets have grown exponentially, by 25% per year over the last 25 years.

Randy Martin, “What Difference do Derivatives Make? From the Technical to the Political Conjuncture”, Culture Unbound, Volume 6, 2014: 189-210:193.

7 Cooper, Melinda. "Turbulent Worlds: Financial Markets and Environmental Crisis." Theory, Culture &Society 27, no. 2-3 (2010): 167-90: 173-78.

8 Already by 2002 Oil markets were the second largest futures market and one of the largest derivatives markets across the global exchanges.

“Derivatives and Risk Management in the Petroleum, Natural Gas, and Electricity Industries” Energy Information Administration U.S. Department of Energy Washington, DC 20585, October 2002 Available at: https://sites.hks.harvard.edu/hepg/Papers/DOE_Derivatives.risk.manage.electric_10-02.pdf Downloaded October 30, 2017.

9 Shiri Pasternak, “Infrastructure and Grounded Authority”, unpublished talk, Concordia University, October 11, 2017.

10 Randy Martin, “What Difference do Derivatives Make? From the Technical to the Political Conjuncture”, Culture Unbound, Volume 6, 2014: 189-210:193.